Aktuelle InSights

Why Sales Commissions Fail in Consulting

By Andy Klose - Associate Partner and Head of Advisory

In many consulting firms, the incentives debate starts with an apparently obvious thought: if senior leaders are expected to win work, why not pay them like salespeople and introduce sales commissions? The logic feels clean—more deals, more pay, more growth. Yet in consulting, this “clean” logic often produces messy outcomes: weaker risk discipline, more internal friction, and—most damaging—reduced client trust. The reason is structural, not ideological. Classic, deal-based sales commissions are designed for transactional selling; consulting is a relational, team-based, judgment-heavy business where value is co-created and realized over time.

The intuitive idea – and where it goes wrong

Product-style sales commissions assume a world of discrete transactions: a salesperson closes a deal, hands it over, and gets paid. The model works because the boundaries are clear—between selling and delivery, between one deal and the next, and between individual contribution and enterprise value.

Consulting rarely fits that template. “Selling” is usually inseparable from diagnosing the problem, shaping the approach, assembling the right team, and standing behind the outcome. When incentives treat consulting like a sequence of independent deals, they encourage behaviors that optimize short-term bookings at the expense of long-term client impact and firm health.

What makes consulting structurally different from transactional sales

Sales commissions become increasingly fragile as offerings become more bespoke and knowledge-intensive. In classic consulting—strategy, operations, HR, organization, transformation—the economics differ in three ways.

First, sales and delivery are integrated. Senior consultants and partners do not merely close; they commit the firm, lead the work, and remain accountable for what was promised.

Second, solutions are heterogeneous by design. Even when proposals reuse methods and modules, each engagement is shaped by client context, politics, risk, data availability, team mix, and outcome uncertainty. This makes “fair” and behaviorally sound deal-level metrics hard to define.

Third, the asset is the relationship, not the transaction. Consulting revenue typically unfolds in waves—diagnosis, design, implementation, follow-on scaling—within a relationship where trust accumulates slowly and can be lost quickly.

A practical rule holds: the more relational and bespoke the work, the less compatible deal-level sales commissions become.

How sales commissions backfire in consulting

Once you view consulting as an interdependent, multi-year value chain, several failure mechanisms become predictable. They reinforce each other, which is why “small” commission schemes often expand into large cultural and economic problems over time.

1. Sales commissions shift the partner mindset from “best answer” to “best-sellable answer”

Consulting buyers pay for judgment and independence. Deal-based sales commissions introduce a strong bias toward whatever is easiest to monetize now. Common patterns include scope inflation, premature solutioning, and a preference for short, high-fee projects over work that builds sustainable client capability. Even if outcomes remain acceptable, clients quickly sense when advice is optimized for revenue rather than relevance. Trust erodes—and trust is the foundation of repeat business.

2. Sales commissions weaken risk discipline and deal quality

Healthy consulting firms say “no” more often than outsiders assume: no to unrealistic timelines, no to misaligned stakeholders, no to underpriced work, no to engagements where success probability is low. Sales commissions can invert that discipline. A large, high-fee, high-risk project becomes personally attractive even if the firm later absorbs the delivery pain, write-offs, or reputational impact. Over time, governance mechanisms—review boards, pricing discipline, delivery readiness checks—get pressured by individuals who are rewarded for closing, not for outcomes.

3. Sales commissions undermine collaboration in a team-based business

Modern consulting delivery is cross-practice and cross-geography. The best client solution often requires multiple senior leaders and specialists to contribute. Sales commissions turn that collaborative system into a contest for “origination credit.” The predictable consequences are territorial behavior (“my client”), reluctance to bring in colleagues if it dilutes payout, and internal negotiation about credit allocation that consumes energy better spent on the client. In a partnership model, internal trust is a strategic asset; sales commissions tax that asset.

4. Sales commissions distort time allocation in multi-task leadership roles

Senior consulting roles are inherently multi-dimensional. Partners and senior leaders must balance business development with delivery leadership, talent development, intellectual capital, and firm stewardship. High-powered incentives tied heavily to sales drive effort toward what is measured and paid, crowding out activities that build long-term advantage—coaching, proposition building, quality assurance, recruiting, and leadership roles. The firm may temporarily see a spike in bookings while quietly accumulating delivery and people risks that surface later.

5. Sales commissions mis-attribute value creation and fuel perceived unfairness

Few consulting wins are attributable to one person. A sale often reflects prior delivery excellence, a long-nurtured relationship, specialist insight, a high-performing team, and the firm’s reputation. Deal-based sales commissions force an artificial choice: either reward the visible “closer” disproportionately, or build complex split models that feel arbitrary and create constant debate. Both outcomes erode perceived fairness—one of the most sensitive levers in professional services cultures.

When commission-like incentives can work (and the boundary conditions)

This is not an argument against variable pay or against rewarding business development. The question is fit: under which conditions do sales commissions align with the operating model?

Commission-like approaches are more viable when most of the following are true:

- Standardized, repeatable offerings (e.g., fixed-scope diagnostics, packaged implementations, training products);

- Clear separation of roles between sales and delivery (dedicated sales teams with limited delivery accountability);

- Lower delivery uncertainty and more predictable scope, timelines, and outcomes;

- Limited cross-team dependency or clearly defined handovers and responsibilities.

Even then, two guardrails are critical: (1) strong controls to prevent overselling or misrepresentation, and (2) commission weightings that signal importance without overwhelming other leadership responsibilities.

In other words, commissions fit best where consulting behaves more like a product business. In bespoke advisory partnerships, those conditions are the exception—not the norm.

What to do instead: incentive principles aligned with consulting economics

If deal-level sales commissions are structurally misaligned, what should consulting firms use to reward and steer senior performance? There is no universal formula, but a consistent set of principles tends to work across partnership and professional services models.

Reward the portfolio, not the deal

Shift the unit of performance from individual transactions to the health of a client portfolio over time. This supports better behavior: disciplined pricing, thoughtful sequencing of engagements, and an emphasis on relationship durability rather than quarterly wins.

Use a balanced set of metrics, not a single “sales number”

Senior performance should reflect the true job, not a simplified proxy. Many firms use a balanced scorecard that includes financial outcomes (revenue and profitability), client outcomes (satisfaction, retention, expansion), people outcomes (team feedback, development, hiring contribution), and firm-building outcomes (thought leadership, proposition development, leadership roles). Business development remains highly valued—but not isolated from delivery quality and stewardship.

Keep “sales credit” as an input to judgment, not an automatic cash engine

Tracking origination and contribution is useful—especially for promotions, recognition, and performance discussions. The risk arises when that tracking becomes a rigid, formulaic payout mechanism. Consulting requires judgment in assessing contribution, risk-taking quality, collaboration, and long-term impact. Incentive systems should preserve room for that judgment.

Protect the partnership logic

Partnerships thrive on shared ownership, mutual accountability, and investment in the next generation. Incentives should reinforce those norms: encouraging leaders to bring the best team to the client, share relationships, develop talent, and protect the firm’s reputation—even when doing so reduces short-term personal upside.

Implications for HR and firm leadership

Incentive design in consulting is not a technical exercise; it is a strategic choice about culture and operating model. HR and leadership teams should treat sales commissions as a “model decision,” not a compensation tweak. Introducing deal-based commissions often forces a firm—implicitly—toward a more individualistic, franchise-like structure with higher internal competition and weaker collective governance.

A more sustainable path typically involves three moves:

- Align incentives with how value is created (team-based, relational, outcome-oriented).

- Design for the long term (multi-year performance, portfolio health, reputation protection).

- Make trade-offs explicit (accepting slightly lower short-term sales intensity in exchange for better collaboration, lower delivery risk, and stronger client relationships).

Conclusion: Don’t install a transactional engine in a relational business

Sales commissions are not inherently “bad.” They are simply optimized for a different context: standardized offerings, separable sales and delivery roles, and value captured in discrete transactions. Consulting—at its core—is the opposite: bespoke problem solving, integrated delivery accountability, and trust built over time.

For consulting firms, the most important question is therefore not, “How do we bolt sales commissions onto our partnership?” It is: Which behaviors and cultural norms does our business model require—and what incentive architecture reinforces those behaviors rather than fighting them? In most advisory partnerships, honest answers to that question lead away from deal-level commissions and toward more balanced, portfolio-based, and collective mechanisms that reward sustainable client impact.

We would be pleased to assist you with any additional inquiries you may have and offer recommendations on how to enhance your organisation’s compensation and incentive models.

Andy Klose is an Associate Partner at Vencon Research International and heads the firm’s advisory unit.

Vencon Research International is a leading provider of compensation benchmarking and research as well as of compensation and performance-related consulting services for professional service firms, especially for audit and tax, management consulting, and IT services firms. Vencon Research International provides services to a full range of clients in more than 75 countries worldwide and is proud to name more than 85% of the world’s major consulting and/or professional services firm its clients.

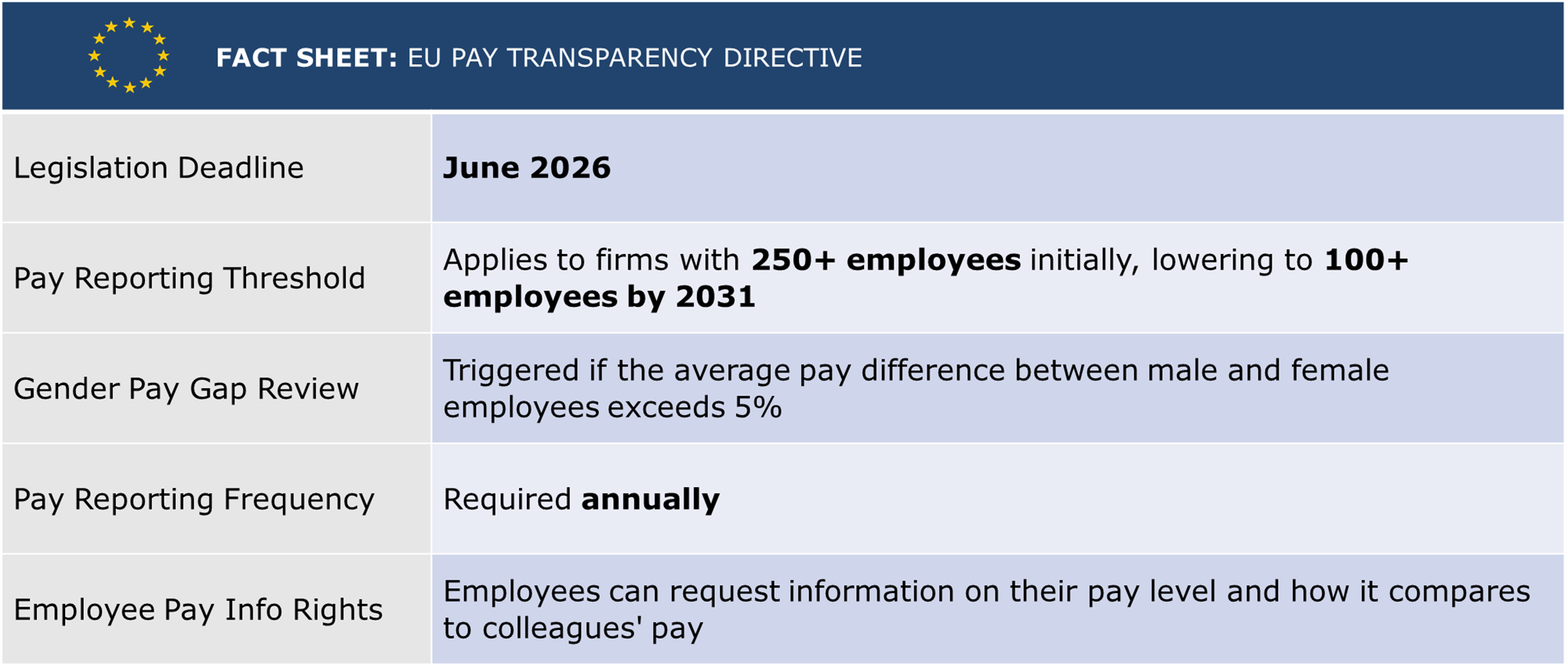

EU Pay Transparency Becomes Law in 2026: What Compensation and HR Teams Should Expect

By Shukhrat Iskandar - Client Solutions

The EU Pay Transparency Directive moves into effect in 2026 and represents one of the most significant regulatory changes affecting compensation management in decades. From mid-2026, Member States are required to have transposed the Directive into national law, after which employers will face new, enforceable obligations around pay transparency, reporting, and employee rights to pay information. Designed to strengthen equal pay for equal work or work of equal value and to close persistent gender pay gaps across Europe, the Directive introduces legally binding measures that go beyond most existing national frameworks, reshaping how organisations define, structure, communicate, and justify pay.

Key Requirements of the Directive

Once transposed into national law, the Directive introduces a set of binding obligations for employers across the EU, including:

- Pay transparency in recruitment: Employers must disclose the starting salary or pay range in job advertisements or prior to the first interview, and may not ask candidates about pay history.

- Employee rights to pay information: Employees can request information on their own pay and on average pay levels for comparable roles, broken down by gender.

- Gender pay gap reporting: Employers with 250+ employees must report annually, with the first reports due in 2027. Employers with 150–249 employees will report every three years from 2027. Employers with 100–149 employees will be brought into scope later under phased national timelines.

- Mandatory corrective action: Where a gender pay gap of 5 percent or more cannot be objectively justified, employers must conduct a joint pay assessment and take remedial action.

- Broader discrimination coverage: The Directive explicitly covers intersectional discrimination, and affected employees are entitled to compensation.

EU Member States must transpose these requirements into national law by 7 June 2026, after which enforcement and reporting obligations will apply according to employer size.

Why the Directive Matters

Despite decades of policies aimed at promoting pay equity, the gender pay gap in the EU remains around 12 percent on average. Structural opacity in pay systems has made it difficult for employees to understand how pay is determined and for authorities to detect discrimination. By mandating transparency, the Directive seeks to transform pay equity from principle into practice.

Improved transparency has the potential to generate meaningful benefits. Research by labour unions suggests that even modest reductions in pay gaps could translate into significant annual earnings increases for many workers. Beyond compliance, transparent pay systems also foster trust with employees, strengthen employer brand, and enhance talent attraction.

Current Organisational Readiness

Recent surveys indicate that many organisations are still in the early stages of preparing for the Directive. A 2025 survey of HR professionals in Germany found that only one in three HR managers were familiar with the Directive’s details. Nearly half of respondents expected implementing the changes to take more than six months, and many cited concerns about additional workload and potential internal conflicts. At least ten EU Member States had taken no steps toward implementation by late 2025, while others were in draft or partial stages of preparation.

Implications for Compensation Teams

The Directive has several practical implications for compensation and HR teams:

- Compensation Structure Review and Redesign: Organisations must ensure that pay structures are defensible under transparency scrutiny. Broad pay grades and informal pay practices must give way to clearly documented, objective, and gender-neutral criteria. Pay decisions must align with job architecture and evaluation systems.

- Pay Gap Reporting and Analytics: Teams must collect, analyse, and report pay data by gender and pay category. This requires accurate, governed data, structured processes for analysis, and mechanisms to address pay gaps exceeding five percent without valid justification.

- Recruitment and Job Advertising: Salary transparency now requires organisations to include pay ranges in job postings or provide this information early in the hiring process. Compensation teams must carefully define salary bands to maintain internal equity once disclosed publicly.

- Talent Attraction and Employer Branding: Transparent pay practices can become a competitive advantage, attracting top talent and building trust with employees and candidates.

Practical Steps to Prepare

To meet the Directive’s requirements, organisations should begin preparations immediately:

- Educate HR, legal, finance, and executive teams about the Directive’s scope, timelines, and obligations.

- Audit pay data, job classifications, and pay bands to identify gaps or inconsistencies.

- Update job evaluation methodologies and pay policies to align with objective, gender-neutral criteria.

- Build repeatable processes for ongoing pay gap reporting and data governance.

- Prepare internal communication strategies to ensure transparency changes are understood and culturally supported.

- Consider technology solutions that automate data collection, reporting, and analytics to improve efficiency and accuracy.

Starting these steps early helps avoid rushed implementation and positions organisations for long-term compliance and pay governance improvements.

Challenges to Anticipate

Even with preparation, compensation teams will face challenges:

- Policy complexity as countries may interpret the Directive differently, creating a patchwork of requirements for multinational organisations.

- Incomplete or inconsistent pay data, which can make reporting difficult without strong governance.

- Sensitive internal discussions around pay transparency, requiring careful communication to maintain trust.

Non-compliance carries legal risk and can damage employer brand and employee trust.

Turning Compliance Into Advantage

While the EU Pay Transparency Directive introduces increased scrutiny and workload, it also offers an opportunity. Organisations that approach transparency strategically can strengthen pay governance, improve employee trust, and enhance employer branding. Clear, fair, and well-structured compensation systems will not only meet legal requirements but also provide a competitive edge in attracting and retaining talent.

For compensation teams, the Directive represents a clear mandate: transparency is coming, and the question is whether it arrives as a disruption or as a capability the organisation is ready to lead.

Supporting Pay Structures Under Increased Scrutiny

Vencon Research advises organisations on how to prepare pay structures for the practical realities of pay transparency. Using market-aligned benchmarking data, we help compensation teams test pay ranges, job matching, and progression frameworks against external practice and identify areas of potential exposure ahead of implementation.

Our advisory work goes beyond supplying data. We work with clients to interpret market evidence, assess pay gap risk, and ensure that pay decisions can be clearly explained to employees, leadership, and regulators once transparency requirements apply.

More information on our advisory services is available here.

Download: Middle East & Africa Consulting Market HR Insights 2024-2025

This series of briefs consolidates essential HR indicators for the consulting sector across three markets in the Middle East and Africa: the United Arab Emirates, Saudi Arabia, and South Africa. It provides a comparative view of compensation positioning, workforce structure, career progression, and service line dynamics across the region.

AI Consulting in Practice: Insight & Transformation vs. Implementation & Managed Services

By Mik Bodnar - Business Development

As AI has matured from isolated pilots to enterprise-wide deployment, it has become a central pillar of business change. Consulting firms including Accenture, Deloitte, McKinsey, Bain, EY, KPMG, PwC, IBM, Infosys, TCS, Wipro, and Oliver Wyman have expanded AI-related offerings in response to sustained client demand.

Across firms, these services tend to fall into two broad categories: Insight & Transformation and Implementation & Managed Services. Together, they reflect the strategic and operational sides of AI adoption—defining both what AI should deliver and how it is embedded at scale.

AI Consulting: Insight & Transformation

Definition This segment focuses on setting direction. It covers strategy, governance, ethics, industry perspectives, and workforce change.

Core question What should AI mean for our business?

Strategic AI Consulting

Strategic AI Consulting helps organizations identify where AI can create material value and how it fits into broader operating and growth models. McKinsey’s QuantumBlack unit, for example, supports clients in prioritising high-impact use cases and building adoption roadmaps that extend beyond pilots.

AI Governance, Risk & Ethics

Governance and risk services establish guardrails for responsible AI use, addressing compliance, transparency, and ethical considerations. Deloitte’s Trustworthy AI framework illustrates how firms help clients balance innovation with regulatory scrutiny and reputational risk.

Industry-Specific AI Strategy

AI strategies are increasingly tailored by sector. EY, for instance, advises financial institutions on AI-driven fraud detection while ensuring alignment with regulatory requirements and model risk standards.

Workforce Transformation

Workforce-focused services prepare organisations for AI-enabled ways of working. This includes role redesign, reskilling, and change management. Bain’s work with retailers on AI-supported inventory and demand planning highlights the emphasis on human–AI collaboration rather than automation alone.

AI Consulting: Implementation & Managed Services

Definition This segment focuses on execution—deploying, operating, and scaling AI in day-to-day environments.

Core question How do we make AI work consistently in practice?

AI Implementation & Integration

Implementation services cover the deployment of AI platforms, models, and automation into existing processes. Accenture’s AI Studio, for example, supports the integration of generative AI into customer service functions to improve responsiveness and personalisation.

AI Product & Solution Development

Here, consultants design and build bespoke AI applications, such as predictive analytics tools or domain-specific generative AI solutions. IBM’s work with healthcare providers on clinical data analysis illustrates this product-oriented approach.

Managed AI Services

Managed services focus on ongoing performance, monitoring, and optimisation. Infosys provides managed AI operations for manufacturing clients, ensuring predictive maintenance models remain accurate as conditions and data change.

Data & Cloud Enablement for AI

AI at scale depends on modern data and cloud foundations. TCS supports organisations in migrating legacy systems to cloud environments, enabling more advanced analytics and model deployment.

Why AI Consulting Matters for Firms and Talent Leaders

AI consulting has become a core practice area, combining strategic advisory work with deep technical execution. Yet growth in this space is constrained by talent availability. Demand for consultants who can bridge business context and advanced analytics continues to exceed supply.

For HR and compensation leaders, access to reliable market data on AI consulting roles is therefore critical. Salary benchmarks support competitive pay structures, internal equity, and retention—particularly as firms compete not only with peers but also with technology companies and startups. Without clear market reference points, consulting firms risk losing scarce AI talent just as these capabilities become central to client value delivery.

AI transformation places new demands on roles, skills, and pay structures. Vencon Research provides HR advisory services alongside compensation benchmarking to help consulting firms make data-backed workforce and pay decisions.

Middle East Consulting: Talent Market and Compensation Insights

By Andy Klose - Associate Partner

The consulting industry in the Middle East, particularly in the United Arab Emirates (UAE) and in the Kingdom of Saudi Arabia (KSA), has experienced a period of rapid growth post-COVID-19. However, recent economic shifts – especially budget cuts in Saudi Arabia’s public sector – have significantly affected management consulting companies operating in the region. While consulting companies in both the UAE and KSA continue to seek sustainable growth, they are facing challenges related to talent acquisition, retention, and compensation structures. This paper explores the key trends in the consulting industry, with a focus on their impact on the talent market and firm operations.

Saudi Arabia: The Epicentre of Consulting Demand

The Kingdom of Saudi Arabia remains the most significant market for consulting services in the region, particularly within its semi-public and government sectors. Many consulting companies have built their business models around serving Saudi clients, and the recent budget cuts have had a profound impact:

- Demand for consulting services has declined across various government projects.

- Most consulting companies have seen their growth slow down, with only a few maintaining the pace of previous years.

- Achieving ambitious revenue and profitability targets has become increasingly difficult for consulting companies.

Despite these challenges, Saudi Arabia remains a crucial market, and consulting companies are adjusting their strategies to adapt to the new landscape.

Increasing Sophistication of Clients and Changing Project Expectations

Clients in the region, from both the private and the public sector, are evolving in their approach to consulting services, which may have an impact on how consulting companies operate and compete:

Key Trends in Client Expectations

- Higher Sophistication: Clients demand deeper expertise and more tailored solutions from consulting companies (including more expertise with regards to the needs of SMEs).

- Longer Project Timelines: Consulting projects are taking longer to execute as clients scrutinize deliverables more closely.

- Shift Toward Smaller Firms: More clients in the region seem to be open to working with boutique consulting companies instead of relying solely on big brand names, creating additional competitive pressure from below.

- Implementation-Focused Consulting: Clients require more than just PowerPoint presentations; they need consulting companies with strong execution and operational expertise.

- Capability Building: Clients seek support in developing internal skills and knowledge instead of continuously outsourcing these capabilities to external consultants.

Implications for Consulting Firms

To succeed in this evolving environment, consulting companies should:

- Strengthen their ability to execute strategies beyond “pure” strategy or advisory work.

- Invest in training programs that help their clients develop in-house expertise.

- Offer practical, hands-on solutions rather than theoretical recommendations.

- Differentiate themselves through specialized expertise rather than relying solely on brand recognition.

Talent Market Pressures in the UAE

Unlike the KSA, the UAE consulting market is facing an overheating talent market with:

- Stagnant Compensation: Consulting salaries are said to have “maxed out”, making it difficult to keep increasing financial incentives as in the recent past. One consulting firm reported that a 5-8% pay increase for every promotion is no longer sustainable from a cost perspective.

- Employee benefits Under Review: As a result of these cost pressures, benefits were mentioned to be a “key differentiating factor” to be increasingly cost effective.

- Rising Cost of Living: The higher cost of living in Dubai and Abu Dhabi is putting pressure on consulting companies to increase allowances, which in turn is affecting profitability. In particular, the cost of accommodation was cited as a critical factor, with the rent for a two-bedroom apartment now as high as a villa with a garden would have been a few years ago. The cost of international schools has also risen significantly.

- Layoffs and Hiring Freezes: Some consulting companies have stopped and delayed hiring or even laid off staff to control costs and improve margins. It was mentioned that firms were more rigorous in their recent performance evaluations than in previous years, letting go of underperformers.

- Shift in Hiring Strategies: Also, some consulting companies are becoming more selective, hiring specialized talent for client or project-based needs rather than generalist consultants. Hiring for IT-related consulting services and subject matter expertise remains at high levels.

The result is a strategic shift in workforce allocation, with more firms opting to place or to hire consultants in the KSA instead of the UAE, where local talent is increasingly available. Also, it was said several times that consulting firms are focussing in the near term more on enhancing their benefits packages as the main differentiator in the talent market.

Evolving Workforce Strategies in Saudi Arabia

The Kingdom of Saudi Arabia has seen a notable improvement in the availability of junior consulting talent. Consulting companies that have invested in strong graduate and internship programs are benefiting from a steady pipeline of entry-level consultants. However, the mid-to-senior level talent pool remains highly competitive:

- Government Sector Competition: While there is no shortage of well-educated Saudi labour, many mid-to-senior-level consultants are being poached by government entities offering attractive compensation packages, leading to high attrition rates. Beyond better pay, many professionals are drawn to government roles for a better work-life balance.

- Localization Pressures: Saudi clients, particularly in the public sector, increasingly prioritize local hires and cultural alignment. This includes:

- Fluency in Arabic.

- Understanding of Saudi business customs.

- Strong local networks for business development.

To address these challenges, some consulting companies are taking innovative approaches to hiring senior-level talent:

- Hiring Senior Consulting Staff from Outside Consulting: Some firms are bringing in senior candidates from industry roles in the hope that they can provide valuable client connections. However, failure rates seem to be high, often due to a lack of sales acumen and consulting expertise.

- Increasing Local Presence: Consulting companies are pressured to have “troops on the ground” to compete for major government contracts. The Saudi government requires firms to demonstrate a local commitment, including adherence to Saudization quotas (40% of staff being Saudi nationals).

Compensation and Workforce Mobility Challenges

As consulting companies adapt to the evolving landscape, compensation strategies are also changing:

- High Costs for Senior Expats: The shortage of mid- to senior-level talent has forced consulting companies to rely on expatriates. However, relocating expats from the UAE to the KSA is expensive, as Saudi Arabia is still considered a “hardship location” from an expat's perspective. And it was said that hiring an expat to work in the KSA would cost 1.25 times more than hiring a Saudi national.

- Reduced Willingness to Relocate: Several international consulting companies noted that they receive many applications for relocation to the UAE from other countries. Once in the UAE, expats are also more inclined to stay, as one firm put it, “This is the highest paying region (in addition to no income tax and a comfortable lifestyle). Everybody wants to come and nobody wants to leave”.

- Dual Contracts for Expats: To mitigate costs, some consulting companies employ dual contract structures:

- A significant portion of the salary is paid in the UAE, where the consultant’s family resides.

- A smaller portion is paid in Saudi Arabia, where the consultant works for 3-4 days per week.

- Alternative Talent Pools: Some consulting companies have started flying in consulting staff from lower-cost countries from Egypt, Jordan, and Lebanon. However, this approach presents challenges such as:

- Visa and work permit complexities.

- Additional allowances required for travel and accommodation.

- Higher attrition rates due to (longer) travel chore and equality concerns.

The Future of Consulting in the Middle East

The Middle East consulting industry is undergoing a transformation driven by economic shifts, talent dynamics, and localization requirements. Consulting companies may adapt their strategies to remain competitive by:

- Investing in Local Talent Pipelines: Strengthening internship and graduate programs to develop homegrown consulting talent.

- Balancing Compensation and Cost Management: Rethinking expat pay structures and leveraging innovative mobility solutions like dual contracts.

- Enhancing Local Market Access: Hiring (senior) professionals with deep local connections while ensuring they have the necessary consulting skills and sales acumen.

- Optimizing Workforce Deployment: Using a mix of onshore, nearshore, and offshore talent to manage costs while maintaining service quality.

- Aligning with Client Expectations: Adapting to client demands for:

- More implementation-driven consulting.

- Stronger internal capability-building efforts.

- IT-related consulting services and subject matter expertise.

- Broader acceptance of smaller consulting firms as credible advisors.

- By proactively addressing these challenges, consulting firms can position themselves for sustained success in both the UAE and KSA markets.

We would be pleased to assist you with any additional inquiries or questions you may have.

Andy Klose is an Associate Partner at Vencon Research International and heads the firm’s consulting unit.

Vencon Research International is a leading provider of compensation benchmarking and research as well as of compensation and performance-related consulting services for professional service firms, especially for audit and tax, management consulting, and IT services firms. Vencon Research International provides services to a full range of clients in more than 75 countries worldwide and is proud to name more than 85% of the world’s major consulting and/or professional services firm its clients.

Consulting Faces Intensified Talent Competition from Tech and Finance

By Mik Bodnar - Business Development

Consulting firms are facing unprecedented competition for talent as tech companies and financial institutions lure top candidates with lucrative packages. Entry-level analysts, digital specialists, and data experts are increasingly weighing opportunities outside consulting, forcing firms to rethink compensation, career development, and workplace flexibility to attract and retain the best professionals.

Rising Salaries Reflect Market Pressure

The competition for talent between consulting firms and the tech and financial services sectors has intensified in recent years. Vencon Research data shows that consulting salaries, particularly for entry-level analysts and specialist roles, are being adjusted upward to remain competitive with the lucrative packages offered by technology companies and investment banks.

While consulting firms traditionally attracted graduates with the promise of diverse project exposure and rapid career progression, they now face direct competition for the same pool of quantitative thinkers, digital strategists, and subject matter experts who are equally sought after in fintech, data science, and corporate strategy roles. Boutique consultancies, unable to match the largest firms or banks on base pay, are differentiating through culture, flexibility, and work-life balance, positioning themselves as attractive alternatives for professionals seeking purpose and autonomy.

Roles Most Affected by Talent Mobility

The roles most likely to transition from consulting into tech and finance are entry-level analysts and mid-level managers with specialized expertise in areas like data analytics, cybersecurity, and financial modeling. Senior partners and managing directors, by contrast, tend to remain within consulting due to the unique equity and client-ownership structures of the profession.

Recruitment trends highlight how consulting, finance, and tech are converging on similar talent pools. We see this trend relfected in demand for benchmarking across sectors. Consulting firms are expected to increase full-time and internship hiring in 2025 after a slowdown in 2024, reflecting renewed demand for advisory services. Finance firms, meanwhile, are rethinking recruitment by broadening strategies to digital platforms and specialized networks to attract candidates with both technical and ESG expertise. Tech companies continue to lead in skills-based hiring, with focus on critical skills such as AI, data analytics, and cybersecurity, but consulting firms are also investing heavily in these candidates.

Across industries, flexible work arrangements and strong employer branding are now essential to attract candidates, with hybrid and flexible models becoming decisive factors in recruitment success.

Global Talent Hubs Intensify Competition

Geographically, the competition is most pronounced in global talent hubs such as the United States, the United Kingdom, Germany, and Singapore, where consulting firms, banks, and tech giants all recruit from the same elite universities and professional networks. In these markets, the challenge for consulting firms is not only to match compensation benchmarks but also to craft a compelling narrative of career development and cultural differentiation that resonates with a new generation of professionals.

Beyond pay, consulting firms can deploy non-financial levers such as hybrid work models, sabbatical programs, and transparent promotion criteria to appeal to talent who value stability and culture as much as compensation. Thus benefits packages are increasingly in focus, and we see a corresponding uptick in benchmarking for these non-financial rewards.

Compensation Remains a Central Battleground

Ultimately, compensation remains a central battleground. Tech and finance firms often lead with higher base salaries, equity participation, and performance bonuses, while consulting firms emphasize structured career paths, training, and international mobility. Strategies for consulting firms include raising entry-level packages to prevent attrition to tech startups or offering retention bonuses for mid-level managers with digital expertise.

For consulting HR leaders, the implication is clear: To compete effectively, market data must be used to identify critical pay gaps, selectively adjust pay scales for critical roles, and emphasize non-financial differentiators such as culture, flexibility, and career development. Partnering with a specialized benchmarking provider like Vencon Research can ensure your firm attracts and retains the right talent while staying ahead of industry trends.

Benchmarking-Daten, die wirken

Um fundierte Entscheidungen über Vergütungspakete in Ihrem Bereich treffen zu können, benötigen Sie die aktuellsten Daten.