Latest InSights

From Support to Core: The Rise of Delivery Centers in Consulting

By Gunjan Kalwani - Rewards Intelligence & Insights

The consulting industry is constantly evolving in response to changing client needs. Traditionally focused on strategic advice delivered by small, specialized teams, consulting firms are now increasingly responsible for implementing large-scale transformations, building technology platforms, and operating data-driven systems.

At the core of this shift is the expanding role of delivery centers. These are centralized hubs supporting projects through analytics, tech development, research and knowledge management. Once seen primarily as a support function, they are now integral to a consulting firms’ global operating models.

As their role shift, firms are placing greater emphasis on compensation for the delivery center workforce to maintain productivity, competitiveness and scalability.

Redefining the Delivery Center

Delivery centers have evolved from limited support functionality into integrated capability hubs that combine analytics, engineering, research, and knowledge management within a single operating layer. Their remit now extends far beyond slide production or background research.

They play a direct role in hypothesis testing, model development, platform buildout, and increasingly, in client implementation. In parallel, they underpin internal capability building—maintaining knowledge assets, supporting proposal development, and enabling cross-office collaboration at scale.

Firms such as Accenture and the Big Four have long operated global delivery networks and are constantly expanding. Strategy firms such as Boston Consulting Group and Bain & Company have also expanded their capability networks to support more technical and research driven engagements.

Geographically, these networks continue to concentrate in markets such as India, Poland, the Philippines, and Mexico. However, location strategy is becoming more nuanced—balancing cost with specialization, attrition risk, and proximity to key client markets.

From Support Function to Operating Model

The novelty of the delivery center model lies in how it reshapes the economics of consulting.

Historically, leverage was driven by pyramidal team structures within a single geography. Today, leverage is increasingly driven by the interaction between client-facing consultants and distributed capability pools. This creates a dual workforce model: one optimized for client engagement, the other for scalable execution.

This shift introduces new complexities:

- Role fragmentation: Traditional consulting roles are being decomposed into more specialized skill sets (e.g., data engineering, machine learning, UX design).

- Blended team structures: Project teams now span multiple geographies and cost bases, requiring tighter coordination and clearer role definition.

- Different productivity curves: Output is no longer measured purely in billable hours, but in throughput, reusability of assets, and speed of delivery.

In effect, delivery centers are not just supporting consulting work—they are redefining how it is produced.

Compensation Design in a Distributed Workforce

As delivery centers mature into a core part of the consulting operating model, compensation can no longer be managed as a simple extension of traditional consulting pay structures. The underlying workforce is fundamentally different—more specialized, more location-sensitive, and more exposed to external talent markets beyond consulting.

This requires a shift from benchmarking as a periodic exercise to compensation design as an ongoing, structured process.

Two challenges stand out:

- Role definition and comparability Delivery center roles often sit at the intersection of consulting, technology, and operations. Standard job titles rarely map cleanly to external benchmarks. Without precise job matching, compensation decisions risk being anchored to the wrong talent markets, leading to either overpayment or retention challenges.

- Location-sensitive pay structures Geographic arbitrage remains a factor, but it is no longer the sole driver. Talent scarcity, skill depth, and attrition risk vary significantly within and across locations. Effective compensation design needs to reflect these nuances, rather than applying broad location-based discounts.

In this context, benchmarking becomes an input into a broader set of decisions: how roles are structured, how pay bands are defined, and how progression is managed across both consulting and delivery center career paths.

Firms are increasingly using this data to answer more strategic questions—where to build capabilities, which roles to prioritize, and how to maintain a coherent employee value proposition across a globally distributed workforce.

The result is a more deliberate approach to compensation: one that reflects the complexity of the delivery center model rather than forcing it into legacy structures.

Implications for Consulting Firms

The rise of delivery centers introduces a more industrialized layer to consulting—one that requires the same level of rigor in workforce planning as seen in technology or operations-heavy industries.

Firms that treat delivery centers as a homogeneous, cost-driven function risk underinvesting in critical capabilities or mispricing their services. Conversely, those that actively manage these workforces—through precise role definition, targeted benchmarking, and continuous capability assessment—are better positioned to scale without eroding margins.

This is particularly relevant as demand for advanced analytics and AI-related work continues to accelerate. The competition is no longer just between consulting firms, but with technology companies drawing from the same talent pools.

Closing Thought

Delivery centers have moved beyond their original mandate. They are now a defining feature of how consulting firms operate, compete, and grow.

The challenge is no longer whether to build these capabilities, but how to manage them effectively within a global, multi-layered workforce. That requires a more sophisticated approach to benchmarking—one that reflects the reality of hybrid roles, distributed teams, and rapidly evolving skill demands.

Firms that get this right are not just optimizing costs; they are reshaping their delivery model to align with where the industry is heading.

As delivery center models continue to evolve, firms need a clearer understanding of how roles, capabilities, and pay structures compare across markets. Vencon Research supports consulting firms with targeted benchmarking and advisory, helping ensure compensation frameworks reflect the realities of a distributed workforce. Get in touch to discuss how this applies to your organization.

Download: 2026 Expected Salary Increases in the Consulting Industry

2026 Expected Salary Increases in the Consulting Industry

These concise overviews provide:

- A consulting-specific picture, representing real estimates gathered first-hand from consulting firms in the local market.

- A picture of country wide expected salary increases, based on data from third-party research.

Vencon Research conducts compensation benchmarking studies for over 70 countries worldwide. Should you require further information on the summaries included or additional data for different countries, please contact us.

The EU Pay Transparency Directive Is Not a Reporting Exercise

The countdown to the transposition of the EU Pay Transparency Directive in June 2026 has already started. For many organisations, the most visible requirement is the obligation to report gender pay gap data and provide employees with access to certain pay information.

This has led to a common initial reaction: build the reporting. But reporting is not the system. It is the output of the system.

The directive was designed precisely to make pay discrimination easier to identify and enforce by linking transparency across several different mechanisms. Reporting sits at the end of that chain. Compliance depends on whether the underlying pay structure, decision logic, and governance framework can withstand scrutiny.

In practice, that means organisations must be able to explain why pay differences exist, how roles are compared, and which criteria determine pay progression. Without those foundations, reporting can quickly surface gaps that cannot be objectively justified neither towards officials nor to employees.

Vencon Research supports organisations’ readiness efforts for the directive across the full lifecycle: from initial diagnostics through structural design, operational implementation, internal communication and reporting.

Why the Directive Goes Beyond Pay Gap Numbers

The directive introduces a broader architecture of transparency obligations that work together.

These include:

- defining categories of workers performing the same work or work of equal value

- establishing objective criteria for pay-setting and pay progression

- providing employees with the right to request pay information

- ensuring salary transparency in recruitment

- producing gender pay gap reporting

- conducting joint pay assessments when unexplained gaps persist

Each of these elements relies on the others. For example, gender pay gap reporting requires organisations to calculate average pay differences between men and women within categories of workers performing equal work or work of equal value.

If those categories are poorly defined—or if job architecture is inconsistent—the resulting comparisons can be misleading or difficult to defend.

Similarly, when employees request pay information about their category, organisations must be able to clearly demonstrate how pay levels and progression decisions are determined.

In other words, transparency forces organisations to make their pay systems explicit, consistent, and auditable.

Many organisations are therefore starting with a structured readiness assessment to understand where their current pay systems may face challenges under the directive.

The Hidden Risk: Escalation Mechanisms

One of the most important aspects of the directive is what happens after pay gaps are identified.

If a gender pay gap of 5% or more appears within a worker category and cannot be objectively justified, employers may be required to carry out a joint pay assessment with employee representatives.

This introduces a form of escalation pressure. Organisations must be able to demonstrate:

- how pay decisions were made

- whether objective criteria were applied consistently

- what corrective actions are required if structural issues are identified

Preparing for these scenarios cannot happen once reporting is already underway. The underlying governance and documentation processes must already be in place.

Preparing early for these escalation scenarios, both analytically and operationally, is becoming a core focus for organisations working toward directive compliance.

Why a Modular Approach Is Often Necessary

Because the directive touches multiple aspects of the pay system, organisations rarely face a single isolated problem.

Instead, they typically need to address several interconnected questions:

- Is the underlying HR and payroll data structured in a way that supports reliable analysis?

- Are job roles and levels defined clearly enough to enable meaningful equal-value comparisons?

- Are pay-setting and progression rules documented and consistently applied?

- Are HR teams and managers prepared to communicate pay ranges and criteria transparently?

- Is there a clear governance process for responding to information requests or investigating potential gaps?

- Which guidelines, policies and communication materials will have to be created, reviewed or changed?

Attempting to solve only the reporting requirement often leaves these questions unanswered.

For that reason, many organisations are beginning to approach the directive as a series of structured building blocks rather than a single compliance project.

Vencon Research works with organisations to design pragmatic implementation roadmaps that address these elements step by step while aligning with the directive’s timelines.

Building the Foundation: Data and Diagnostics

The first step is usually establishing a reliable fact base.

Pay transparency requirements rely on the ability to combine data from several systems, including HRIS, payroll, organisational structure data, and job information. In many organisations these datasets exist, but definitions and calculation rules differ across functions.

Creating a consolidated and auditable dataset allows organisations to:

- define pay components consistently

- standardise FTE and working-time adjustments

- segment employees into meaningful analytical groups

- reproduce calculations reliably for future reporting

Once this foundation exists, organisations can begin to assess the current state of pay equity. This typically involves analysing gender pay gaps across multiple segments—such as job families, levels, locations, or contract types—and distinguishing between structural drivers and potentially unexplained differences.

The purpose of this diagnostic is not only to measure current gaps but also to identify areas where the organisation may face higher scrutiny under the directive.

Vencon Research supports organisations in building auditable pay datasets and conducting detailed pay equity diagnostics aligned with directive requirements.

Defining “Work of Equal Value”

One of the most technically complex aspects of the directive is the concept of equal value comparisons.

Organisations must be able to compare roles across functions using gender-neutral criteria such as:

- skills

- effort

- responsibility

- working conditions

- contributions

In practice, this requires a coherent job architecture and job evaluation logic that allows roles from different functions to be assessed within the same framework.

For example, a marketing role and a finance role may be very different operationally, but the directive requires employers to demonstrate whether they represent comparable value in terms of responsibility, complexity, and required capabilities.

Without a structured job architecture, these comparisons become extremely difficult to defend.

Designing robust job architectures and evaluation frameworks is therefore a key step in preparing organisations for equal-value comparisons under the directive.

Embedding Transparency Into HR Processes

Even with a clear structure in place, transparency only works if the organisation’s day-to-day processes align with it.

This often requires reviewing how pay decisions are made across several areas:

- hiring and salary offers

- promotions and role changes

- annual pay reviews

- variable pay and allowances

Managers need clear guidelines on how pay ranges are applied and how exceptions are documented. Organisations also need to define how pay-setting and progression criteria are communicated to employees in a consistent and understandable way.

This is where communication and enablement become critical. Transparency requirements affect not only HR teams but also recruiters, line managers, and senior leadership.

Vencon Research supports organisations in embedding transparent pay governance into HR processes, policies, and manager decision frameworks.

Preparing for Reporting and Employee Requests

Once the underlying structure and processes are in place, organisations can build the reporting outputs required under the directive.

These typically include:

- gender pay gap calculations across defined worker categories

- documentation explaining the methodology used

- governance processes for reviewing and approving results

- templates for responding to employee pay information requests

Equally important is preparing for scenarios where gaps require further investigation or remediation.

Having predefined approaches for documentation, corrective action, and stakeholder involvement allows organisations to respond quickly if reporting results trigger additional obligations.

Vencon Research helps organisations establish repeatable reporting frameworks and prepare operational responses for employee information requests and potential joint pay assessments.

A Structural Shift in Pay Governance

The EU Pay Transparency Directive represents a shift in how pay systems are expected to operate.

Historically, many organisations relied on implicit practices and informal decision-making frameworks that worked reasonably well internally but were rarely documented in detail.

Transparency changes that expectation.

Pay systems must now be designed so that they can be explained, justified, and audited. This requires stronger data foundations, clearer role structures, and more explicit governance around pay decisions.

For organisations that address these elements systematically, the directive becomes manageable. Those that focus only on the final reporting step may find themselves dealing with much more complex questions once transparency exposes how their pay system actually works.

Organisations beginning their preparation now have the advantage of building these foundations in a structured way before reporting obligations come into force.

Preparing for the EU Pay Transparency Directive? Vencon Research supports organisations across the full preparation journey—from pay equity diagnostics and job architecture to governance frameworks and reporting readiness. Get in touch to discuss how we can support your organisation.

India’s Unique Remuneration Structure: Considerations for Rewards Benchmarking

By Deepali Bist, MBA - Client Solutions

In India, compensation is not constructed as a single consolidated salary figure. It is deliberately segmented into statutory-linked pay, structured allowances, and performance-related incentives. This layered design reflects regulatory requirements, tax considerations, and long-standing market practice.

For consulting firms, where compensation represents the largest operating cost and a central talent lever, benchmarking accuracy depends on more than headline numbers. It depends on whether remuneration components are defined and compared consistently. Selecting and standardising the right elements directly influences the reliability of market positioning conclusions.

Global benchmarking frameworks often rely on simplified compensation categories to enable cross-country reporting. While efficient at scale, these frameworks do not always align with the architecture of Indian pay structures. Without localisation, structurally different packages may be treated as comparable, affecting both external benchmarking and internal band calibration.

At Vencon Research, we observe that benchmarking quality in India is closely linked to how precisely remuneration components are interpreted within the local statutory and market context.

The Architecture of Consulting Compensation in India

In Indian strategy and management consulting firms, compensation typically consists of three principal layers:

- Basic Salary

- Allowances

- Performance Bonus

Each serves a distinct financial and regulatory function.

Basic Salary

Basic salary generally represents around half of fixed compensation. It serves as the statutory anchor for:

- Provident Fund (12% of Basic)

- Gratuity accrual (~4.81% of Basic)

Because these obligations are legally defined, the level and treatment of Basic pay have direct cost and compliance implications. Adjustments to Basic salary do not merely shift internal pay mix — they influence statutory exposure.

Allowances

Allowances typically form the remaining portion of fixed pay and may include House Rent Allowance (HRA) and other special allowances. While sometimes viewed as flexible elements, they are part of fixed cash compensation and materially affect take-home pay outcomes through tax optimisation.

In benchmarking datasets, allowances are occasionally treated inconsistently — particularly where global reporting templates do not distinguish between Basic and total fixed pay.

Performance Bonus

Variable pay is a meaningful component in consulting, particularly at post-MBA and senior levels. Performance bonuses link compensation to individual, team, and firm outcomes, and can represent a substantial share of Total Cash Compensation (TCC).

Employer Statutory Contributions

Employer contributions such as Provident Fund and Gratuity provisions increase Total Cost to Company (CTC) but do not affect immediate take-home pay. For benchmarking purposes, distinguishing between:

- Employee cash compensation, and

- Employer statutory cost

is essential.

Dearness Allowance (DA), while relevant in certain public-sector contexts, is generally not applicable in private-sector consulting firms and should not be assumed to form part of standard structures in this sector.

Why Component Definition Drives Benchmarking Accuracy

Inconsistent definitions of compensation elements can quickly distort market comparisons. A frequent issue arises around the interpretation of “base pay.” Some firms define base as Basic salary only, while others define it as total fixed pay (Basic + Allowances). Without normalisation, benchmarking outputs may misrepresent relative positioning.

Two firms may report different CTC figures while delivering similar employer cost structures and take-home outcomes. Conversely, similar headline figures may conceal materially different:

- Statutory exposure

- Bonus weighting

- Fixed-to-variable pay ratios

Without component-level clarity, these structural differences remain hidden.

Statutory alignment is equally important. If Basic pay is set at an unusually low proportion of fixed compensation, Provident Fund and Gratuity obligations may be understated. Alternatively, including discretionary or non-cash elements within total compensation figures can inflate perceived competitiveness.

These distortions typically arise not from error, but from applying simplified definitions to a market with structural particularities.

The Global–Local Translation Challenge

Multinational consulting firms operating in India often rely on centralised reward frameworks designed for global consistency. These frameworks usually categorise pay into a limited set of universal components — such as:

- Base Salary

- Variable Pay

- Benefits

In the Indian context, however, “Base” is not a single undifferentiated figure. It includes internal layers that carry statutory consequences. Allowances that are integral to fixed pay may be treated as peripheral benefits in global systems. Pension logic applied elsewhere may not align with India’s statutory 12% Provident Fund requirement.

Without translating global templates into Indian compensation architecture, benchmarking comparisons may appear aligned while concealing structural misinterpretation.

Ensuring Market Relevance in Indian Benchmarking

Compensation structures in India are shaped by:

- Tax legislation

- Labour and wage code frameworks

- Statutory contribution rules

- Market-driven take-home pay expectations

Accurate benchmarking therefore requires:

- Clear distinction between Total Cash Compensation (TCC) and broader CTC constructs

- Alignment with statutory definitions for correct employer cost modelling

- Normalisation of Basic, Allowances, and Variable Pay across participating firms

When remuneration elements are standardised appropriately, benchmarking data becomes materially more reliable and comparable across consulting firms.

Vencon Research’s Approach

Vencon Research’s benchmarking framework for consulting firms in India is built around component-level precision.

Compensation data is disaggregated into:

- Basic Salary

- Allowances

- Variable Pay

Employer statutory contributions are aligned with Indian legal definitions, and cash compensation analysis is separated from non-cash benefits benchmarking. All submissions are normalised into a unified Total Cash Compensation model, reducing distortions caused by inconsistent CTC interpretations.

This approach allows both domestic and multinational consulting firms to maintain global reporting consistency while ensuring local accuracy.

Structural Precision Enables Reliable Decisions

In the Indian consulting market, remuneration structure materially influences statutory exposure, employer cost, and perceived competitiveness. Benchmarking that does not account for these structural layers risks drawing conclusions from non-comparable data.

When compensation components are clearly defined, standardised, and normalised, firms gain a more accurate view of their market position and can make better-informed reward decisions.

Vencon Research supports strategy and management consulting firms in aligning global reward frameworks with Indian compensation architecture. If you are reviewing your salary benchmarking approach in India, we would welcome a discussion on how structural normalisation can improve the precision of your market insights.

Expected Salary Increases 2026: Global Consulting Outlook

Analysis by Irina Kvirikadze - Rewards Intelligence & Insights

Research findings from Vencon Research indicate that salary increases in 2026 are expected to be more moderate compared with the high-inflation years of the recent past.

Organizations across the consulting industry are adjusting compensation strategies in response to easing inflation, ongoing economic uncertainty, and structural changes in workforce management such as AI-driven automation. Rather than broad base-salary increases, employers are increasingly emphasizing variable pay, promotion-driven adjustments, and holistic total rewards offerings.

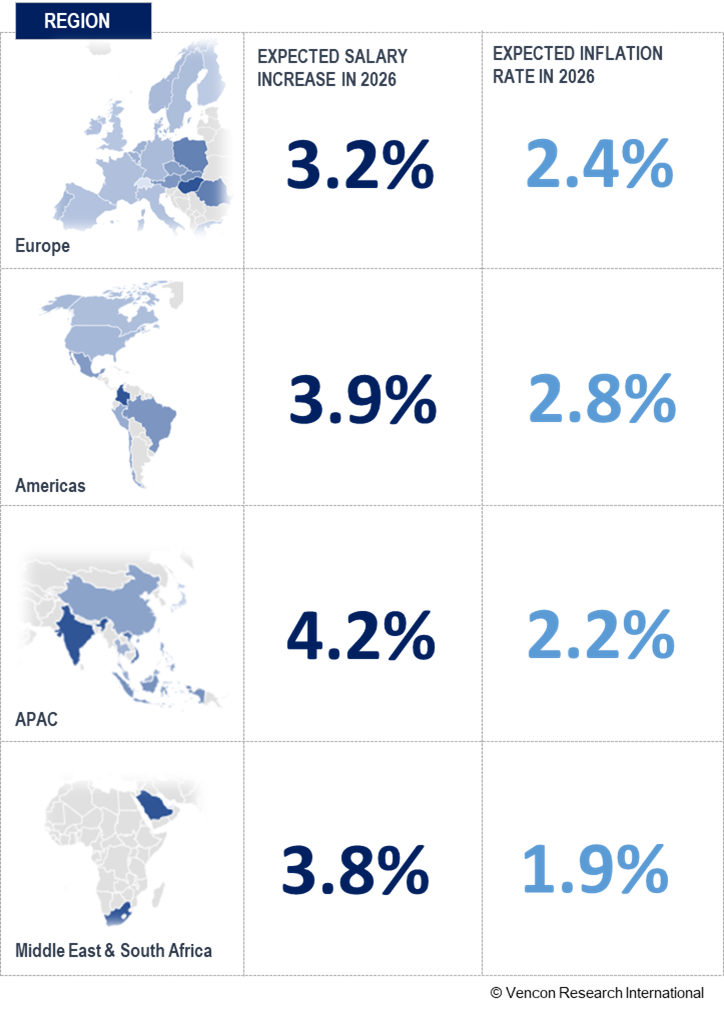

Globally, average salary increases in the consulting industry are projected at 3.7% in 2026, while inflation is expected to stand at 2.4%. This represents a clear slowdown compared with 2025, when salary growth was projected at 4.5%, reflecting a more cautious and targeted approach to pay management.

Regionally, the APAC region expects the highest salary increases, at 4.2%, while Europe is likely to see comparatively lower increases at 3.2%. Expected Inflation rates are highest across the Americas at 2.8%.

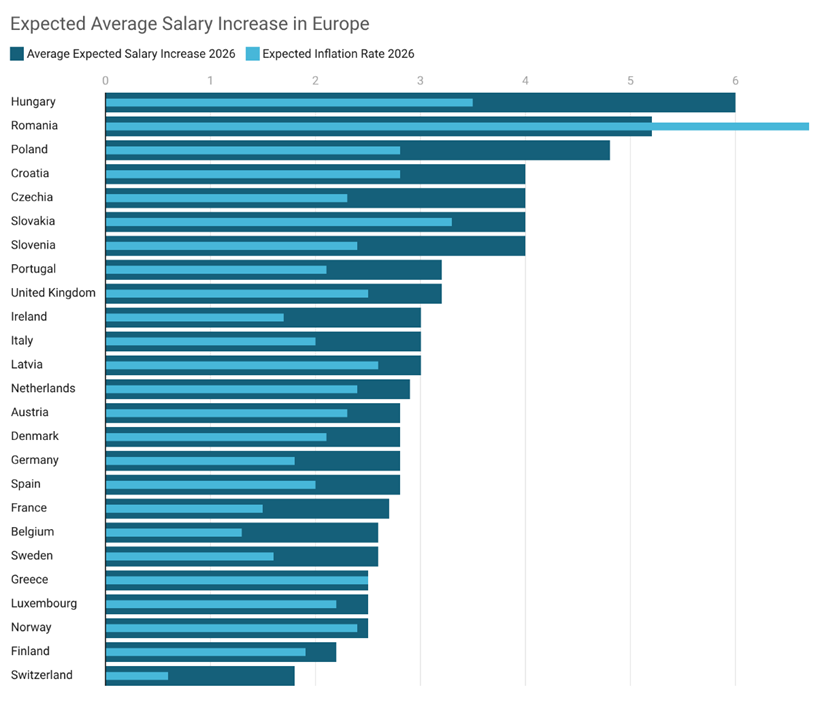

Expected Salary Growth: Europe

In Europe, salary increases are expected to range from 1.8% to 6%, broadly aligned with inflation levels that vary significantly by country. Core markets such as Germany, France, Spain, and the United Kingdom are projected to see moderate increases between 2.7% and 3.2%, while higher growth is anticipated in parts of Central and Eastern Europe, particularly Hungary and Romania, where inflationary pressures remain elevated.

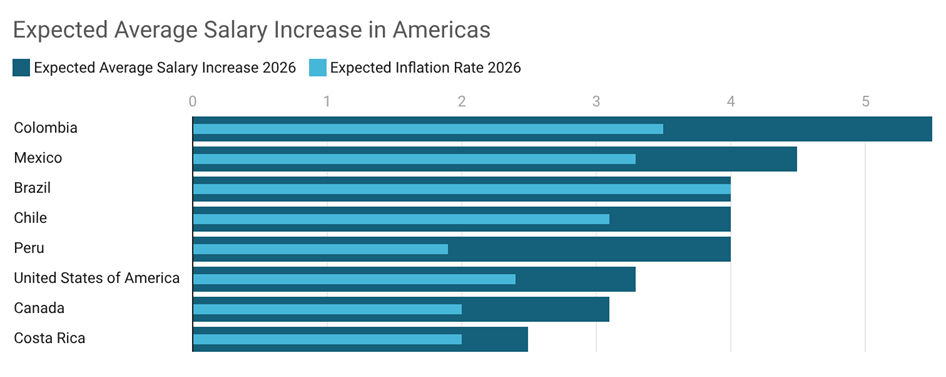

Expected Salary Growth: Americas

Across the Americas, average salary increases in 2026 are projected at 3.9%. Latin America continues to outpace North America, led by Colombia, Mexico, and Brazil, while salary growth in the United States and Canada is expected to remain moderate at just above 3%. Argentina has been excluded from regional averages due to ongoing inflation volatility.

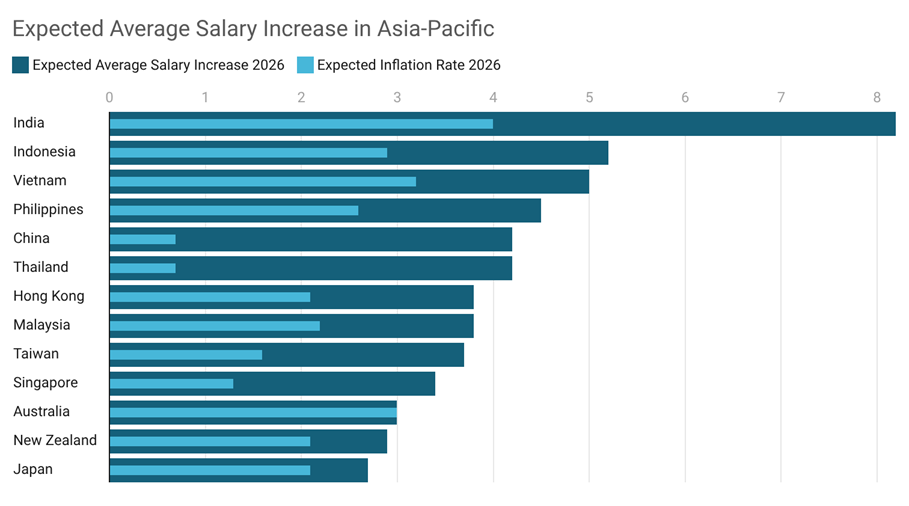

Expected Salary Growth: APAC and MENA

In APAC, salary growth is expected to remain robust and broadly in line with 2025 levels, ranging from 2.7% to 8.2%. India continues to stand out as the strongest growth market globally.

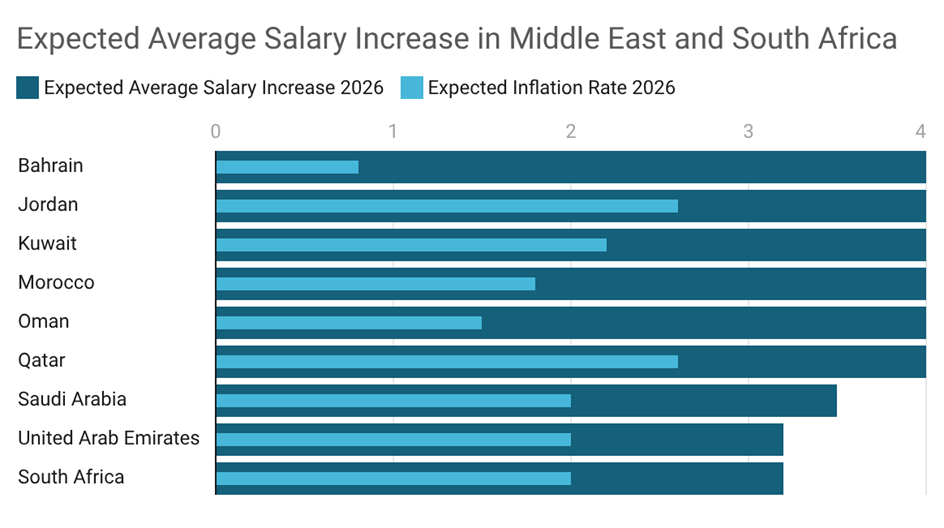

In the Middle East and Africa, salary increases are projected to soften compared with last year, with most major markets clustering around the low-to-mid 3% range.

Overall, the 2026 outlook points to a return to more normalized salary growth, with employers prioritizing flexibility, performance differentiation, and total rewards optimization over uniform pay increases.

Vencon Research provides consulting firms with precise, industry-specific compensation benchmarking, ensuring they stay competitive in a rapidly evolving market. Our research includes further detailed insights into salary increases for 2025 by country, line of business, and career level, helping firms understand pay trends and make informed compensation decisions.

Learn more about how Vencon Research can support your firm’s pay strategy.

HR Trends in Consulting for 2026

As consulting firms plan for 2026, HR leaders face a complex set of pressures. Economic uncertainty, regulatory change, persistent talent shortages and the practical integration of AI are all influencing how consulting firms design roles, manage costs and develop their people.

These challenges are cumulative rather than isolated. Pay and progression decisions are more transparent, workforce models are more varied, and expectations around productivity and performance continue to rise. HR strategy in consulting is increasingly central to sustaining competitiveness and executing business models.

Drawing on Vencon Research’s work with consulting firms globally, alongside selected external research, the following HR trends outline how people strategy in the consulting industry is evolving heading into 2026.

1. Pay Transparency and Regulation as Core HR Priorities in Consulting

Pay transparency is now a central consideration for consulting firms. Regulatory developments, including the EU Pay Transparency Directive and similar initiatives elsewhere, are accelerating the need for clearer pay structures, defined ranges and consistent progression criteria.

In practice, this places pressure on job architecture, levelling and job matching. Vencon Research frequently observes that transparency initiatives expose inconsistencies in role definitions that were previously less visible. For consulting firms operating across multiple geographies, aligning local practices with global frameworks adds further complexity.

As a result, pay transparency is shaping not only reward strategy, but also governance, communication and trust.

2. Workforce Planning in a Low-Growth, High-Volatility Consulting Market

Many consulting firms are entering 2026 with more cautious growth assumptions. Demand remains uneven across sectors and geographies, while cost discipline has become a sustained priority rather than a temporary response.

HR functions are placing greater emphasis on flexible workforce planning, redeployment and internal mobility. Hiring decisions are increasingly guided by near-term demand signals rather than long-range growth forecasts. Vencon Research sees firms investing more time in aligning capacity, skills and cost structures across practices.

Workforce planning is becoming a continuous, data-driven process rather than an annual exercise.

3. AI as a General-Purpose Capability in Consulting Firms

AI is increasingly embedded across consulting roles, grades and practices. By 2026, consultants are expected to use AI-enabled tools for research, analysis, drafting and insight generation as a standard part of their work.

This has implications for HR. Role profiles now assume baseline AI literacy, with differentiation driven by judgment, problem framing and client interaction rather than task execution. Vencon Research observes early incorporation of AI expectations into capability frameworks and performance evaluations.

AI is reshaping what effective consulting work looks like, even where job titles remain unchanged.

4. Evolving Consulting Operating Models Beyond the Pyramid

The traditional consulting pyramid is being supplemented by more diverse talent models. Core consultants increasingly work alongside subject-matter experts, delivery centres, contractors and alliance partners.

This evolution reflects both cost pressures and the growing need for specialised skills. However, it introduces challenges around performance management, engagement and equity. HR processes designed for homogeneous populations are being adapted to support differentiated talent segments without undermining cohesion.

Consulting firms are moving towards more modular and flexible operating models.

5. Rethinking Reward Beyond Utilisation and Billable Hours

Utilisation remains a critical metric in consulting, but it is no longer sufficient alone. As firms invest in intellectual property, platforms and reusable assets, they are exploring ways to recognise non-billable but value-creating contributions.

Vencon Research’s compensation benchmarking shows increasing variation in how firms reward asset development, reuse and broader client outcomes. These changes raise questions around measurement, attribution and fairness, particularly in team-based environments.

Reward strategy is becoming more closely tied to how firms create value, not just how hours are billed.

6. From Leveraged Labour to Asset-Enabled Consulting Models

Closely linked to reward is the shift towards more asset-enabled consulting. AI and automation accelerate this transition, but the underlying change is structural.

Roles increasingly combine client delivery with contributions to tools, methodologies and platforms. Vencon Research observes early differentiation between delivery-led roles and hybrid roles blending advisory, product and commercial responsibilities.

Over time, this trend will continue to influence career paths, grading structures and promotion criteria.

7. Reconfiguring Learning and the Consulting Apprenticeship Model

The widespread adoption of AI and digital tools has changed how junior consulting work is performed. Tasks traditionally used to build foundational skills are increasingly automated or augmented.

Consulting firms are rethinking how learning and development are structured, introducing more formal development pathways, earlier responsibility and clearer expectations around skill progression.

Preserving the strengths of the apprenticeship model while adapting it to new working patterns remains a central HR challenge.

8. Attracting and Developing Scarce and Interdisciplinary Talent

Skill shortages continue to affect consulting firms, particularly in areas such as data, technology, sustainability, risk and regulatory advisory. These roles often combine technical and strategic capabilities that do not align neatly with traditional consulting career models.

Vencon Research sees firms combining targeted hiring with greater emphasis on reskilling and internal mobility. Career frameworks are being adjusted to support deeper expertise alongside broader consulting development.

Talent strategy is increasingly shaped by scarcity rather than surplus.

9. Integrating Technology and AI Acquisitions into Consulting Firms

Acquisitions remain a key route for capability building, particularly in AI and digital services. Integration, however, remains challenging. Differences in culture, pace and reward expectations can create friction within partnership-led firms.

HR is playing a greater role in redesigning job families, performance frameworks and progression paths to accommodate hybrid consulting-technology roles. Organisational design is becoming as important as retention in determining success.

Integration is no longer viewed as a short-term issue, but an ongoing management challenge.

10. Governing AI as Part of Professional and Risk Standards

As AI becomes embedded in client delivery, consulting firms are formalising expectations around its use. Regulatory scrutiny, client expectations and reputational risk are driving clearer policies and accountability.

HR’s role includes embedding AI-related competencies into role profiles, supporting training and certification, and clarifying responsibility for appropriate use. In many firms, AI governance is treated as an extension of professional standards.

This reflects a broader shift towards explicit risk management in people strategy.

11. Leadership Capability in Hybrid and Distributed Consulting Firms

Hybrid working models are now well established, but their implications for leadership continue to evolve. Leading distributed teams requires new capabilities around performance management, coaching and engagement.

Research from organisations such as Gartner consistently highlights leadership development as a priority for CHROs. In consulting, effective leadership is increasingly linked to productivity, retention and culture.

Leadership capability is a critical lever in sustaining performance.

12. Re-Anchoring Culture and Learning in Hybrid Consulting Environments

With less reliance on physical proximity, consulting firms are taking deliberate steps to build culture and support learning. Informal knowledge transfer no longer happens by default.

Vencon Research observes increased investment in structured onboarding, coaching and hybrid collaboration practices. While flexibility remains a key attraction and retention factor, maintaining consistency and connection across the firm requires ongoing effort.

Culture and learning are increasingly treated as design challenges rather than by-products of co-location.

13. Building Talent for Sustainability, Climate and Resilience Practices

Demand for sustainability, climate, ESG and resilience-related advisory continues to grow across the consulting industry. Clients increasingly expect firms to combine strategic insight with technical and regulatory expertise, prompting many to scale dedicated practices or embed sustainability capabilities across service lines.

For HR, this creates challenges that do not fit neatly within traditional consulting models. Sustainability and climate roles often require interdisciplinary profiles, combining consulting skills with scientific, engineering, regulatory or data expertise. Firms are responding through a mix of targeted external hiring and structured reskilling of existing consultants.

As these practices mature, HR functions play a central role in defining job architecture, career paths and reward frameworks that support growth.

HR Trends in Consulting: Looking Ahead to 2026

These HR trends demonstrate a continued shift towards greater clarity, discipline and integration in people strategy. Regulatory change, evolving operating models and technology adoption reinforce the need for coherent job architecture, reward structures and development pathways.

For consulting firms, HR is no longer limited to support or compliance. It is central to shaping how consulting work is delivered, how talent is developed, and how value is created in a complex, competitive environment.

Contributors

- Erwin Harbauer - Managing Director / Partner

- Andy Klose - Associate Partner

- Shukhrat Iskandarov - Client Solutions Manager

Vencon Research works closely with consulting firms to translate these insights into practical decisions. Whether you are assessing your workforce model, reviewing reward frameworks, or designing career paths, our benchmarking and advisory services can provide the data, analysis and guidance needed to act with confidence. Contact us to discuss how we can support your HR strategy for 2026 and beyond.

Benchmarking Data that Works

In order to make informed decisions about compensation packages in your field, you need the latest data at

your fingertips.