By Deepali Bist, MBA & Osas Ohenhen - Business Development

In compensation benchmarking, timing is everything. One often overlooked but critical factor influencing accuracy is a firm’s financial and salary review cycles — of which the financial year (FY) is often a key reference point.

For consulting firms (and indeed for many organizations), understanding the timing nuances is not just an accounting formality; it is a strategic cornerstone for effective remuneration planning and decision-making.

What Is a Financial Year (FY)?

A financial year (FY) is a 12-month period an organization uses for financial reporting and performance measurement. While some firms align their FY with the calendar year (January–December), others adopt alternative cycles such as:

- April–March (e.g., Big4 India, most UK based consulting firms)

- July–June

- October–September (common among several Big4 firms globally)

These choices typically reflect tax regulations, business seasonality, or internal strategic preferences. As a result, peer firms within the same industry may operate under different FY cycles, which can influence when they set budgets, review salaries, and adjust remuneration components.

Understanding these timelines ensures benchmarking efforts reflect the right data points in the right context.

Why FY Alignment Matters in Compensation Benchmarking

Financial year alignment is crucial for ensuring compensation benchmarking delivers accurate, actionable insights. It affects planning, salary review timing, and remuneration components.

1. Planning & Budgeting

Most firms align salary increases and bonuses with their FY. A mismatch in timing can distort benchmarking insights.

Example: Firm ABC Consulting follows an April 2025–March 2026 FY (FY26) but did not finalize its budget until December 2025. As a result, they only received benchmarking data in April 2026, by which time many peer firms had already reviewed and adjusted salaries.

Consequently, ABC’s benchmarking data appeared inflated or outdated — not because the market had changed dramatically, but because the comparison timing was misaligned.

Best Practice: Firms should synchronize benchmarking cycles with their budgeting and salary review windows to ensure market data reflects the most relevant and current pay decisions.

2. Salary Review Cycles

Salary review cycles vary significantly across firms and markets. Understanding when peers conduct reviews helps maintain competitiveness and prevent attrition.

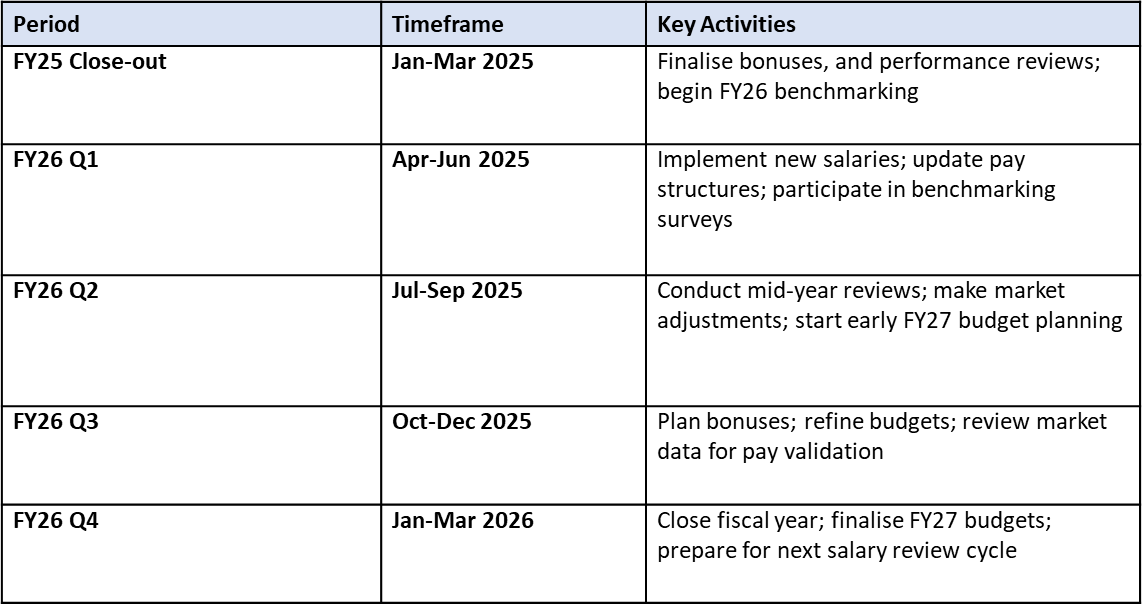

Example: In India and the UK, salary reviews often occur around April, aligning with the April–March FY. So a simple example of how a firm with a financial year spanning April 1, 2025 – March 31, 2026 (FY26) might structure its remuneration planning:

Best Practice: To stay aligned, firms should:

- Identify peer firms’ salary review months within each market.

- Incorporate effective date mapping into their benchmarking framework.

- Use multi-market benchmarking data carefully, ensuring timing equivalence.

3. Remuneration Components

Beyond base salary, FY cycles influence a range of pay elements linked to financial performance, including:

- Bonus pay-outs (individual and company performance)

- Long-term incentives (LTIs)

- Fixed overtime (e.g., Japan)

- Allowances (e.g., India, Mexico, Brazil, Belgium, UAE)

- Gratuity and pension contributions (e.g., India’s PF, Australia’s Superannuation)

- Profit-sharing

These components often follow fiscal performance outcomes, meaning that aligning benchmarking with FY cycles ensures accurate comparisons of total remuneration.

Risks of Overlooking FY in Benchmarking

Overlooking FY differences can lead to:

- Misinterpreted market data

- Mistimed salary reviews

- Inaccurate budgeting

- Loss of top talent

Global HR leaders often face additional complexity due to market-specific pay structures. For instance:

- France: Profit-sharing schemes (Participation and Intéressement)

- Belgium/Luxembourg: Representation allowances

- India: Gratuity and Provident Fund

- Australia: Superannuation

For multinational consulting firms, these considerations are interconnected. Failing to integrate such region-specific components into FY-aligned benchmarking can result in significant data inconsistencies and inaccurate pay comparisons.

Understanding Fiscal Naming vs Salary Validity

There is often confusion between fiscal year naming and salary validity.

For a firm with April 1, 2025 – March 31, 2026 (FY26):

- March 2025: FY25 ends.

- April 1, 2025: New salaries take effect (referred to as 2025 salaries).

- These salaries remain valid until March 31, 2026 (FY26).

In short: Even though the fiscal year is called FY26, the salary adjustments effective April 2025 are 2025 salaries, since they take effect in calendar year 2025.

Understanding this distinction prevents confusion when comparing data across firms using different fiscal and salary naming conventions.

Vencon’s Approach: Turning Timing Complexity into Benchmarking Clarity

At Vencon Research, we recognize that timing alignment is not just administrative — it is strategic. Our experience supporting consulting and professional services firms enables us to help HR leaders:

1. Align Benchmarking Cycles with Firm-Specific FY Structures

- Data Continuity: We collect and refresh data continuously, delivering “point-in-time” reports aligned with clients’ salary review cycles. For example: A survey with data up to June 30, 2025 remains valid through May 2026.

- Data Collection: Our questionnaires capture key timing details — salary effective dates, review periods, and bonus pay-out months — ensuring precise interpretation.

- Market Validity Mapping: We validate each market’s data against local pay cycle trends to prevent temporal distortion.

2. Interpret Market Data in the Correct Timing Context

- Example – Turkey: Due to high inflation and currency volatility, we collect data at a single point (e.g., 31 October 2025) for a realistic snapshot.

- Example – Bulgaria: With euro adoption scheduled for 1 January 2026, our pre-transition survey provides insights into how peers manage conversions, rounding, and timing communication.

3. Build Efficient, Data-Driven Review and Budgeting Processes

We help clients integrate benchmarking outcomes directly into budget planning tools, ensuring that FY-linked pay reviews and financial planning are data-driven, consistent, and actionable.

Strategic Implications

While fiscal calendars and salary reviews may appear technical, their implications for compensation benchmarking are strategic.

For consulting firms seeking to strengthen remuneration planning, improve timing, and retain high-performing talent, aligning compensation benchmarking with your financial year is a crucial practice. Reach out to Vencon Research to ensure your next review cycle is built on accurate, industry-specific data.